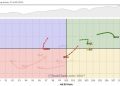

Toronto Dominion Bank (NYSE:TD) stock tumbled over 5% Thursday after reports of a forthcoming $3 billion settlement related to its anti-money-laundering practices in the United States.

According to the Wall Street Journal, citing sources familiar with the matter, TD’s U.S. unit is expected to plead guilty to charges that it failed to implement proper systems to combat money laundering.

The WSJ said the financial penalties are expected to be implemented as the bank “failed to properly monitor money laundering by drug cartels.”

The anticipated settlement will involve hefty penalties and growth restrictions for TD in the U.S.

As part of the agreement with regulators, the publication says the Office of the Comptroller of the Currency (OCC) is expected to impose an asset cap on TD’s retail business, preventing any expansion above a certain level.

The WSJ adds that the U.S. Department of Justice (DOJ) and the Treasury’s Financial Crimes Enforcement Network (FinCEN) will also place independent monitors to oversee the bank’s compliance with the settlement terms.

The monitor from FinCEN is expected to remain in place for four years, according to sources familiar with the matter.

TD Bank’s reported settlement follows a serious investigation that unveiled deficiencies in its anti-money-laundering protocols. The WSJ said Federal authorities discovered that a Chinese criminal organization had laundered millions through TD branches in New York and New Jersey.

The investigation prompted U.S. regulators to scrutinize the bank’s internal controls, which ultimately derailed its planned $13.4 billion acquisition of First Horizon (NYSE:FHN) in May 2023.

In light of the regulatory challenges, TD has been restructuring its anti-money-laundering and investigations divisions, making several key hires to improve its systems.

Despite these efforts, the bank’s stock has suffered, with shares down this year, contrasting sharply with the broader market’s recovery.